|

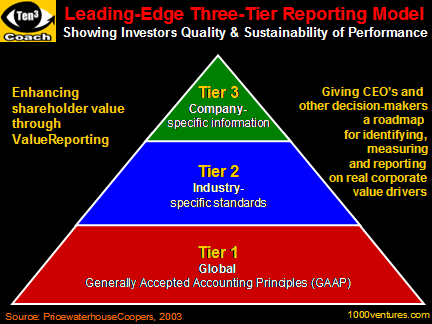

Why Three-Tier

Model?

To operate effectively, investors need the

ability to assess the quality and sustainability of corporate

performance. In the

new economy, users of corporate reports want current financial data

augmented by insightful information on a company's core value drivers.

To meet investors' requirements, you must understand what type of

information they require and how best to communicate it.

The three-tier model proposes a framework for

corporate reporting that responds to the demands of your key stakeholders.

To achieve enhanced shareholder value, ValueReporting gives senior decision

makers a roadmap for identifying, measuring, and reporting on real corporate

value drivers. It comprises three tiers of information which represent an

integrated model for improving corporate transparency.

Three Tiers of Information

These tiers are not separate, discrete

reporting levels, but instead represent and integrated model for

improving corporate transparency.

Tier 1: Generally Accepted

Accounting Principles (GAAP)

Various GAAPs exist, however there is now a

trend towards utilization of International Accounting Standards (IAS) as

the preferred choice. If you wish to enhance your ability to access

global capital markets, you need to provide information that conforms to

internationally accepted standards in order to give investors the

ability to compare your company with your international counterparts.

Tier 2:

Industry-Specific Standards

Increasingly, investors want to compare

companies in an industry sector by reviewing more than just information

mandated by generic financial reporting standards. Your company will

benefit by supplementing GAAP with industry-specific data that can be

used to compare performance among peers.

Tier 3: Company-Specific

Information

Certain important metrics are not included in

tiers one and two as they are unique to the company. The

strategy

employed to

exploit targeted opportunities within a specific market is one

example. Such information is to be provided to investors in this tier. |